I actually have several friends who have written off the use of credit cards entirely in their lives. After paying off ridiculous amounts of debt accrued during their college years, they promptly closed out every account and cut up every card they had.

Luckily my family is not part of that overwhelmingly disheartening statistic. In fact, my family has found ways to use credit cards to our advantage to save money and get free stuff. Here are a few examples along with some tips on how you can use credit cards in a fiscally responsible way to help reach your frugal living goals.

1. Limit Your Number of Credit Cards - I get offers all the time for new credit cards. Citibank and Discover must send me at least one or two "You're Pre-Approved!" letters each month. But I already have one major credit card and share another with my husband for household purchases; I don't really need additional cards. Opening too many credit card accounts too quickly, having too many "new accounts" and having too much available credit can take a toll on your credit score. Moreover, having my purse filled to the brim with shiny, new credit cards will only make me tempted to use them, thus spending more - perhaps more than I have available to spend.

|

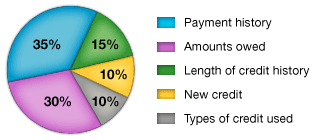

| Breakdown of How Your FICO Score (Credit Score) is Determined |

2. Try to Pay Most (If Not All) of Your Balance Each Month - My credit card statements actually break down the length of time it would take to pay off my balance if I made only minimum payments versus double the minimum payment. The amount I'd pay if I made only minimum monthly payments is typically triple, if not quadruple, the original balance. It's outrageous! Which leads me to the next tip...

3. Don't Charge Something You Can't Afford - If I don't have the cash in the bank to pay for the item I'm purchasing with a credit card, I won't purchase it. There are some rare cases when I use promotional low or no-interest rates to purchase items I plan on paying off over a period of time. But for the most part, if I couldn't have just stopped at the bank and gotten cash to pay for the purchase, I won't swipe my charge card to pay for it either even if I really, REALLY want those fabulous $200 Steve Maddens.

Example 1:

My husband, Jon, and I fell in love with a gorgeous heirloom-style distressed dining room set when shopping at a flea market. The set at the flea market was too badly damaged for us to justify spending what the seller was asking and he wouldn't budge on the price. So Jon and I spent an afternoon price comparing online at a bunch of local furniture retailers. We finally found our set, but at the cost of around $2000, money we didn't have readily accessible. So we approached the sales person at the store with our conundrum and she suggested we open a store charge card to get 0% financing for 5 years. Two-thousand dollars spaced out over 5 years with absolutely no financing fees boils down to less than $35 a month, a reasonable amount of money to budget each month for a set we still love years later.

4. Pay Attention to the Fine Print, Annual Fee and APR - You know those too-good-to-be-true credit card offers? That's exactly it - they're typically too-good-to-be-true. Many credit card companies suck you in with their 0% interest for a promotional period and then whack you with crazy annual percentage rates of upwards of 30%, which can increase dramatically if you miss the payment deadline. Some also have hefty annual fees but no incentives to offset those fees.

Example 2:

Jon frequently travels for work and has been a Marriott Rewards participant since he got his current job. So when we got an offer in the mail for a Marriott Rewards credit card, it was almost a no-brainer to sign up. Although the card comes with a $89 annual fee, we are guaranteed a free night at a hotel within the Marriott chain each year, along with a bunch of other great incentives, such as points for purchases, extra points for stays at Marriott hotels and extra nights for being a "good" credit card user and paying our balance each month. The incentives awarded easily offset the $89 fee we pay each year to have the card. We were able to stay for free after running our Rugged Maniac race last September (and the hotel had free breakfast too!) and we just booked a night for free to attend the birthday of a friend who lives far away. If we had to pay for the hotel stays, we'd spend way more than $89!

5. Establish (and Maintain) Good Credit - Establishing and maintaining good credit through using credit cards in a fiscally responsible way can help you get approved for loans or a mortgage. Because Jon and I have been credit card holders who rarely carry a balance and never miss a credit card payment, we had no trouble at all getting pre-approved for a mortgage when looking to buy a house back in 2009.

Example 3:

Consider the rewards offered by certain credit card companies for making purchases using their card. If you have the cash available to make the purchase, but could receive rewards, additional discounts or other incentives for making the purchase using your credit card, why not do it?

I even pay many of my utility bills using my major personal credit card so I can accumulate points. I had so many points this year, that I was able to get almost $300 in gift cards to give as gifts this Christmas. I was already going to pay those utility bills and had the cash available to pay off my credit card balance each month, so might as well get some incentive for using my card!

Example 4:

After shoveling snow for weeks on end a few years ago, despite a blown-out back, Jon and I decided that we were due to purchase a snow blower to make our lives easier. We budgeted for months, setting aside money for the purchase. When we finally saw one on sale a few months ago, we realized we could save even more by purchasing it using our Lowes card, which offers 5% off all your purchases or special 0% interest financing for purchases over $299. We saved an additional $50 by using our credit card and we immediately paid off our bill with the money we had already set aside.

Here are just a few store cards that offer discounts/rewards. But before you go out and sign up for every card that offers rewards, consider whether you really need the card, will frequently make purchases using it and the effect opening that card will have on your credit score.

- Target offers 5% off your entire purchase if you charge it to your Target Red Card.

- Lowes offers 5% off your entire purchase or 2 financing options when you use your Lowes card.

- Kohls will send you special discounts (15%, 20% or 30% off your order) 12 times a year if you opt to get their Kohls card.

Happy Couponing!

-Coupon Mama Massachusetts

No comments:

Post a Comment